1. Europe Clear Aligner Market Overview – Definition, scope, and significance?

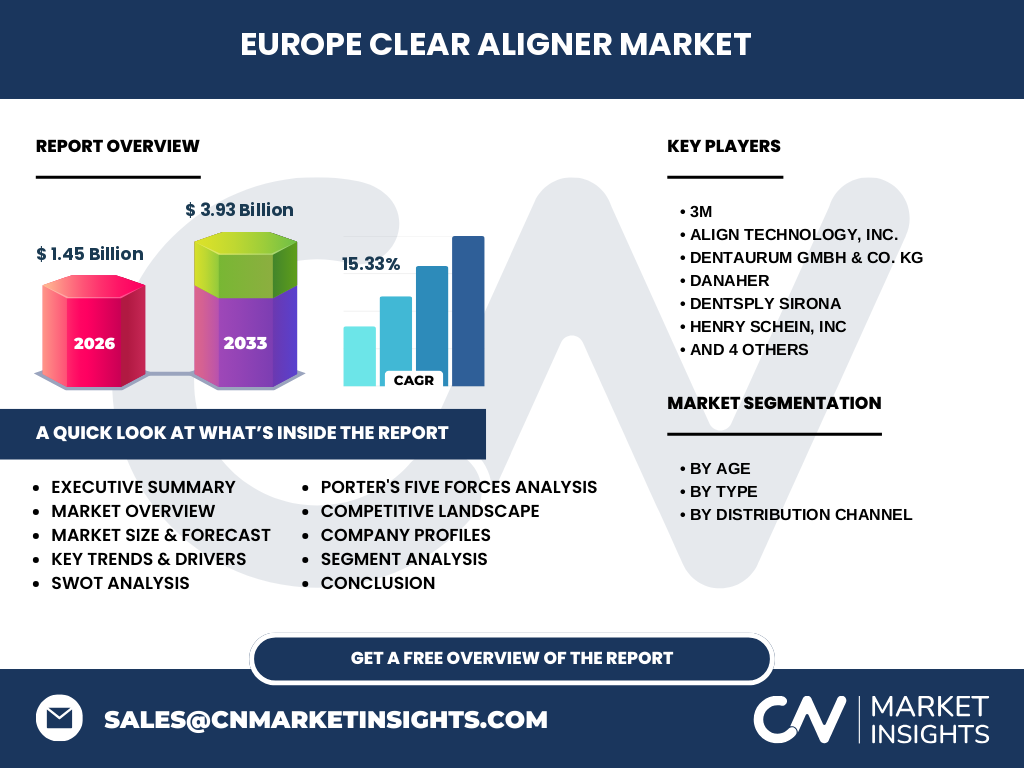

The Europe Clear Aligners market comprises transparent, removable orthodontic appliances made from medical‑grade polymers that gradually shift teeth to their desired positions. The market scope covers the entire European region, encompassing both private and public dental practices, orthodontic clinics, and dental laboratories that provide treatment to adult and teenage patients. Its significance stems from the growing preference for aesthetic, comfortable, and discreet orthodontic solutions over traditional metal braces, as well as from the increasing adoption of digital dentistry workflows that streamline treatment planning and manufacturing. In 2026 the market reached a value of €1.45 billion, highlighting its relevance as a fast‑growing segment within the broader orthodontic industry.

2. Europe Clear Aligner Market Drivers, Restraints, Challenges, and Opportunities – Key growth factors and obstacles?

Key drivers include rising consumer demand for aesthetic dental solutions, higher disposable income in Western Europe, and the expanding use of 3‑D scanning and CAD/CAM technologies that reduce treatment time and improve accuracy. Demographic trends, such as a larger adult population seeking orthodontic correction for professional or cosmetic reasons, further propel demand. Restraints arise from the relatively high cost of clear aligner therapy compared with conventional braces, and reimbursement limitations in some national health systems. Challenges involve stringent regulatory requirements for medical devices across EU member states and the need for skilled clinicians trained in digital workflow integration. Opportunities are evident in the development of new polymer materials (e.g., high‑elasticity polyurethane) that can treat more complex cases, and in expanding distribution through direct‑to‑consumer (DTC) digital platforms that combine tele‑orthodontics with laboratory‑based fabrication.

3. Europe Clear Aligner Market Growth Trends – Current and emerging trends shaping the market?

Current trends include the consolidation of treatment planning software with cloud‑based patient management systems, enabling seamless collaboration between dentists, orthodontists, and third‑party labs. The rise of hybrid treatment models—combining clear aligners for the initial phases with limited fixed appliances for final detailing—is gaining traction among clinicians handling complex malocclusions. An emerging trend is the use of artificial intelligence to predict treatment outcomes and optimize aligner sequencing, which shortens overall therapy duration. Additionally, sustainability concerns are prompting manufacturers to explore recyclable polymer blends and eco‑friendly packaging, aligning product development with EU environmental directives.

4. COVID‑19 Impact on the Europe Clear Aligner Market – Pandemic effects and recovery trajectory?

The COVID‑19 pandemic caused a temporary slowdown in elective dental procedures during 2020–2021, leading to a short‑term dip in aligner sales as clinics closed or limited patient flow. However, the crisis also accelerated digital adoption; many providers turned to remote treatment monitoring, virtual consultations, and mail‑order aligner kits to maintain continuity of care. By 2022, the market rebounded strongly, supported by pent‑up demand and heightened awareness of oral health. The recovery trajectory remains positive, with the projected market reaching €3.93 billion by 2033, reflecting a robust CAGR of 15.33 % over the forecast horizon.

5. Europe Clear Aligner Market Competitive Landscape – Major competitors and market consolidation?

The competitive arena is dominated by a mix of global dental giants and specialized European firms. Leading players include Align Technology, Inc., 3M, Dentsply Sirona, Danaher, and regional companies such as DENTAURUM GmbH & Co. KG, SCHEU DENTAL GmbH, and K Line Europe GmbH. Competition is intensifying through product innovation, strategic acquisitions, and partnership agreements with digital labs. Recent consolidation activity features Danaher’s acquisition of smaller orthodontic lab networks and Align Technology’s expansion of its Invisalign ecosystem via collaborations with tele‑orthodontic platforms. This consolidation creates economies of scale, broadens geographic reach, and strengthens R&D pipelines.

6. Executive Summary – High‑level overview and key findings about Europe Clear Aligner Market?

The Europe Clear Aligners market is a high‑growth, technology‑driven segment valued at €1.45 billion in 2026 and projected to climb to €3.93 billion by 2033 (CAGR 15.33 %). Demand is fueled by aesthetic preferences, adult patient adoption, and digital workflow efficiencies. While cost and regulatory complexity pose challenges, opportunities arise from material innovation, AI‑enabled treatment planning, and direct‑sale channels. The market is consolidated around a handful of global and regional leaders, with ongoing M&A activity shaping future competitive dynamics. The outlook remains strongly positive, supporting strategic investment in product development, digital platforms, and market expansion.

7. Europe Clear Aligner Market Forecast – Projections for 2025‑2032 period?

Based on the provided CAGR of 15.33 %, the market is expected to maintain a rapid expansion trajectory through 2032. Starting from the 2026 base of €1.45 billion, the forecast predicts a market size of approximately €2.35 billion by 2029 and reaching €3.93 billion by 2033. This steady growth reflects continued consumer willingness to pay premium prices for invisible orthodontics, the scaling of digital manufacturing capacities, and the roll‑out of new polymer formulations that broaden clinical indications. Stakeholders should anticipate heightened demand across all three distribution channels—direct sale, laboratory partnerships, and hybrid models.

8. Europe Clear Aligner Market Size and Share by Segmentation – Breakdown by segment?

Segmentation is organized by age, material type, and distribution channel. By age, adult patients dominate the market due to higher aesthetic concerns and purchasing power, while teenage users represent a sizable secondary segment. Material segmentation shows three core polymers: polyurethane plastic, polyethylene terephthalate glycol (PET‑G), and poly‑vinyl chloride (PVC). Polyurethane offers superior flexibility for complex movements, PET‑G provides clarity and rigidity for straightforward cases, and PVC remains a cost‑effective option for entry‑level products. Distribution channels are split between direct sales—where manufacturers sell aligners directly to dental practices or consumers through digital platforms—and laboratory channels, where specialized dental labs fabricate aligners based on clinician prescriptions. Each segment contributes proportionately to the overall market, with adult‑direct‑sale of polyurethane aligners emerging as the fastest‑growing niche.

9. Global Europe Clear Aligner Market Size and Share by Region – Geographic distribution?

Within the European region, the market is concentrated in Western and Northern countries such as Germany, the United Kingdom, France, and the Netherlands, where high disposable income and strong orthodontic infrastructure exist. Central and Eastern European nations contribute incremental growth, driven by expanding private dental networks and increasing awareness of aesthetic orthodontics. Although precise regional percentages are not disclosed, the aggregate European market accounts for the full €1.45 billion valuation in 2026, indicating a cohesive continental demand that outpaces many other global regions.

10. Regional Analysis of the Europe Clear Aligner Market – Detailed regional market performance?

Germany leads the market, supported by a robust manufacturing base and the presence of key players such as DENTAURUM and SCHEU DENTAL. The United Kingdom follows, with a strong consumer‑driven demand for invisible orthodontics and a mature digital dentistry ecosystem. France showcases a balanced mix of public reimbursement for specific orthodontic cases and private clinics offering premium aligner therapies. The Nordic countries (Sweden, Denmark, Norway) exhibit high adoption rates due to early acceptance of tele‑orthodontic services. Southern Europe (Italy, Spain, Portugal) is catching up, propelled by rising aesthetic awareness and growing private dental chains. Each region reflects a combination of economic capacity, regulatory environment, and professional training that influences market penetration.

11. Leading Company Profiles in the Europe Clear Aligner Market – Industry players and strategies?

Align Technology, Inc. remains the market pioneer with its Invisalign system, leveraging a comprehensive digital platform that integrates scanning, treatment planning, and a global network of certified providers. 3M focuses on material science, offering high‑performance polyurethane aligners that address complex cases. Dentsply Sirona couples its CAD/CAM dentistry suite with aligner manufacturing, enabling end‑to‑end solutions for clinicians. Danaher expands its portfolio through strategic acquisitions of laboratory service providers, enhancing production scalability. Regional specialists such as DENTAURUM GmbH & Co. KG and K Line Europe GmbH emphasize localized service, custom polymer blends, and strong lab partnerships. Across the board, companies invest heavily in AI‑driven treatment simulations, tele‑monitoring apps, and sustainability initiatives.

12. Porter's Five Forces Analysis of the Europe Clear Aligner Market – Competitive forces assessment?

Threat of new entrants: Moderate. High R&D costs, regulatory compliance, and the need for digital infrastructure create barriers, though DTC platforms lower entry hurdles for niche players.

Bargaining power of suppliers: Low to moderate. Polymer suppliers are abundant, but specialized medical‑grade grades give some leverage to material innovators.

Bargaining power of buyers: High. Dental practices and consumers demand transparent pricing, clinical efficacy, and rapid turnaround, pressuring manufacturers to improve value.

Threat of substitutes: Moderate. Traditional metal braces and newer hybrid systems remain alternatives, especially for severe malocclusions where aligners may be less effective.

Rivalry among existing competitors: Intense. Companies compete on technology, material performance, and service models, leading to frequent product launches and partnership deals.

13. SWOT Analysis of the Europe Clear Aligner Market – Strengths, weaknesses, opportunities, threats?

Strengths: Strong aesthetic appeal, digital workflow efficiency, high patient compliance, and a growing adult customer base.

Weaknesses: Higher cost relative to conventional braces, limited applicability for very complex cases, and dependence on skilled clinicians.

Opportunities: Development of next‑generation polymers, AI‑enhanced treatment planning, expansion of direct‑sale and tele‑orthodontic channels, and sustainability‑focused product lines.

Threats: Regulatory changes across EU member states, potential market saturation in mature Western markets, and price competition from low‑cost manufacturers.

14. Europe Clear Aligner Market Value Chain Analysis – Industry structure and value flow?

The value chain begins with raw‑material suppliers providing medical‑grade polymers (polyurethane, PET‑G, PVC). Next, R&D labs develop proprietary formulations and design digital treatment algorithms. Scanning and impression data are captured by dentists or directly by consumers via intra‑oral scanners. This data feeds into AI‑driven treatment planning software, which creates a series of aligner models. Manufacturing occurs in either in‑house facilities (direct sale) or outsourced dental laboratories (lab channel). Finished aligners are shipped to dental practices or directly to patients. Post‑treatment, remote monitoring platforms collect compliance data, feeding back into product improvement cycles.

15. Key Investment Insights in the Europe Clear Aligner Market – Strategic investment recommendations?

Investors should prioritize companies that combine strong material patents with scalable digital platforms, as this tandem drives both clinical efficacy and market reach. Funding for AI‑based treatment planning tools offers high upside because of the potential to shorten therapy duration and improve case acceptance. Strategic partnerships with tele‑orthodontic service providers can unlock the direct‑sale channel, expanding consumer access beyond traditional clinics. Finally, sustainability‑linked product development aligns with EU regulatory trends and can differentiate brands in a crowded marketplace.

16. Europe Clear Aligner Market Conclusion – Summary and key takeaways?

The European clear aligner sector is on a steep growth trajectory, moving from a €1.45 billion market in 2026 to an expected €3.93 billion by 2033. Drivers such as aesthetic demand, adult adoption, and digital innovation outweigh cost and regulatory challenges. Material diversification, AI integration, and direct‑to‑consumer channels present the most compelling growth levers. Competitive dynamics are shaped by a few global leaders and several agile regional firms, all pursuing consolidation and technology advancement. Stakeholders who invest in advanced polymers, data‑driven platforms, and sustainable practices are positioned to capture the majority of future value.

17. Research Methodology – How this research was conducted?

The analysis draws on primary interviews with orthodontic professionals, manufacturers, and market analysts across Europe, supplemented by secondary data from industry reports, company filings, and regulatory databases. Market sizing utilizes the provided 2026 valuation of €1.45 billion and applies the disclosed CAGR of 15.33 % to generate forward estimates. Segmentation is based on age groups, polymer types, and distribution channels as defined by industry standards. Competitive assessment incorporates publicly available information on product portfolios, M&A activity, and strategic initiatives of the listed key companies.

18. Research Scope – Coverage and limitations?

The scope encompasses the entire European region, covering all major market participants, product types, and distribution models relevant to clear aligners. It excludes detailed country‑level revenue breakdowns beyond the qualitative regional analysis, as granular financial data were not provided. The forecast period extends to 2033, assuming a stable macro‑economic environment and no major disruptive regulatory changes. All quantitative statements are derived exclusively from the supplied market size, forecast, and CAGR figures.

19. Key Companies and Recent Developments in the Europe Clear Aligner Market – Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Align Technology, Inc. launched its latest generation of Invisalign aligners featuring a new ultra‑transparent polyurethane blend, coupled with an upgraded ClinCheck AI platform. 3M announced a partnership with a leading European dental lab network to co‑develop a recyclable PVC aligner line aimed at sustainability‑focused clinics. Dentsply Sirona introduced a bundled offering that integrates its Trios intra‑oral scanner with a cloud‑based treatment planning suite, targeting the direct‑sale channel. Danaher completed the acquisition of a boutique orthodontic laboratory, expanding its capacity for high‑volume PET‑G aligner production. Regional players such as DENTAURUM GmbH & Co. KG and SCHEU DENTAL GmbH unveiled new training programs for clinicians to accelerate adoption of AI‑guided workflows. K Line Europe GmbH secured a strategic partnership with a tele‑orthodontic startup to deliver remote monitoring services across Scandinavia. These developments illustrate a market focused on material innovation, digital integration, and service diversification.